All Categories

Featured

Table of Contents

Various policies have different maximum levels for the amount you can spend, up to 100%., is added to the cash value of the policy if the indexed account shows gains (generally determined over a month).

This indicates $200 is contributed to the money value (4% 50% $10,000 = $200). If the index falls in worth or remains consistent, the account internet little or nothing. There's one benefit: the insurance holder is secured from sustaining losses. Although they carry out like protections, IULs are not thought about investment safeties.

Having this suggests the existing cash worth is safeguarded from losses in an inadequately carrying out market., the client does not get involved in an unfavorable crediting price," Niefeld stated. In other words, the account will not lose its original cash value.

Variable Universal Life Insurance Quotes

For example, somebody that develops the policy over a time when the market is choking up could end up with high premium payments that don't contribute at all to the cash money value. The plan can after that potentially lapse if the premium settlements aren't made in a timely manner later in life, which can negate the point of life insurance policy altogether.

Insurance coverage firms usually set optimal involvement rates of much less than 100%. These constraints can restrict the actual rate of return that's credited towards your account each year, no matter of just how well the plan's hidden index executes.

However it is necessary to consider your personal risk tolerance and financial investment objectives to make sure that either one lines up with your total approach. The insurance firm generates income by maintaining a part of the gains, including anything above the cap. The attributing price cap may restrict gains in a booming market. If the capitalist's money is bound in an insurance plan, it can potentially underperform other investments.

The capacity for a greater rate of return is one advantage to IUL insurance policy policies compared to other life insurance policy plans. However, larger returns are not guaranteed. Returns can as a matter of fact be lower than returns on other products, depending on exactly how the market does. Insurance holders have to approve that risk for possibly higher returns.

In the event of policy cancellation, gains become taxable as income. Fees are generally front-loaded and built into complicated crediting price calculations, which may perplex some capitalists.

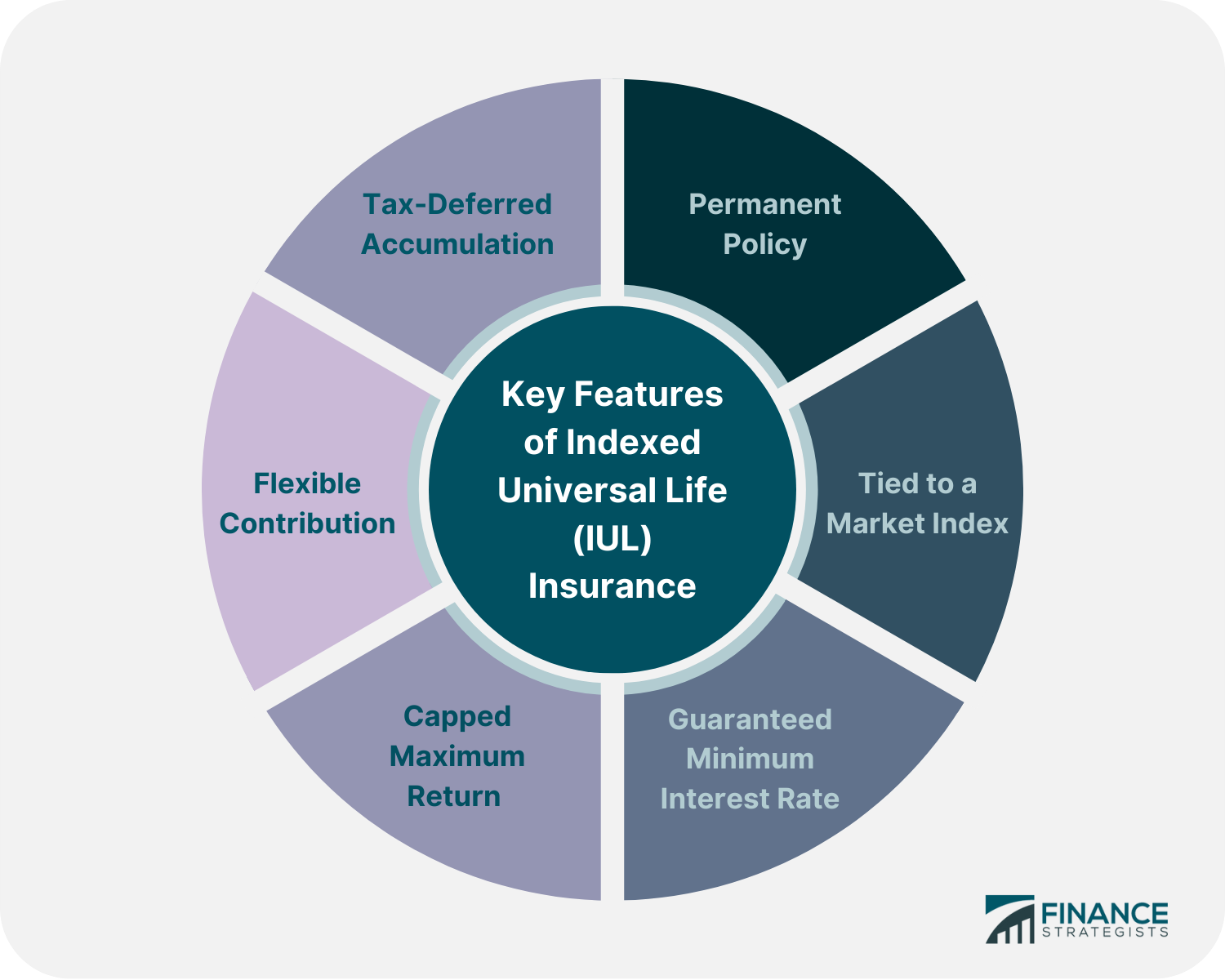

Sometimes, taking a partial withdrawal will certainly likewise completely minimize the fatality benefit. Terminating or surrendering a policy can bring about more prices. Because situation, the cash surrender value might be less than the cumulative premiums paid. Pros Provide higher returns than various other life insurance policy plans Enables tax-free capital gains IUL does not decrease Social Security advantages Policies can be created around your threat cravings Cons Returns capped at a particular level No ensured returns IUL might have greater charges than other policies Unlike various other kinds of life insurance policy, the worth of an IUL insurance policy is linked to an index connected to the stock exchange.

What Is Guaranteed Universal Life Insurance

There are several other kinds of life insurance coverage policies, explained listed below. Term life insurance policy uses a set advantage if the insurance policy holder passes away within a set amount of time, typically 10 to 30 years. This is just one of the most economical types of life insurance, along with the simplest, though there's no money worth accumulation.

The policy acquires worth according to a taken care of schedule, and there are less fees than an IUL insurance plan. Variable life insurance comes with even more adaptability than IUL insurance coverage, meaning that it is also extra complex.

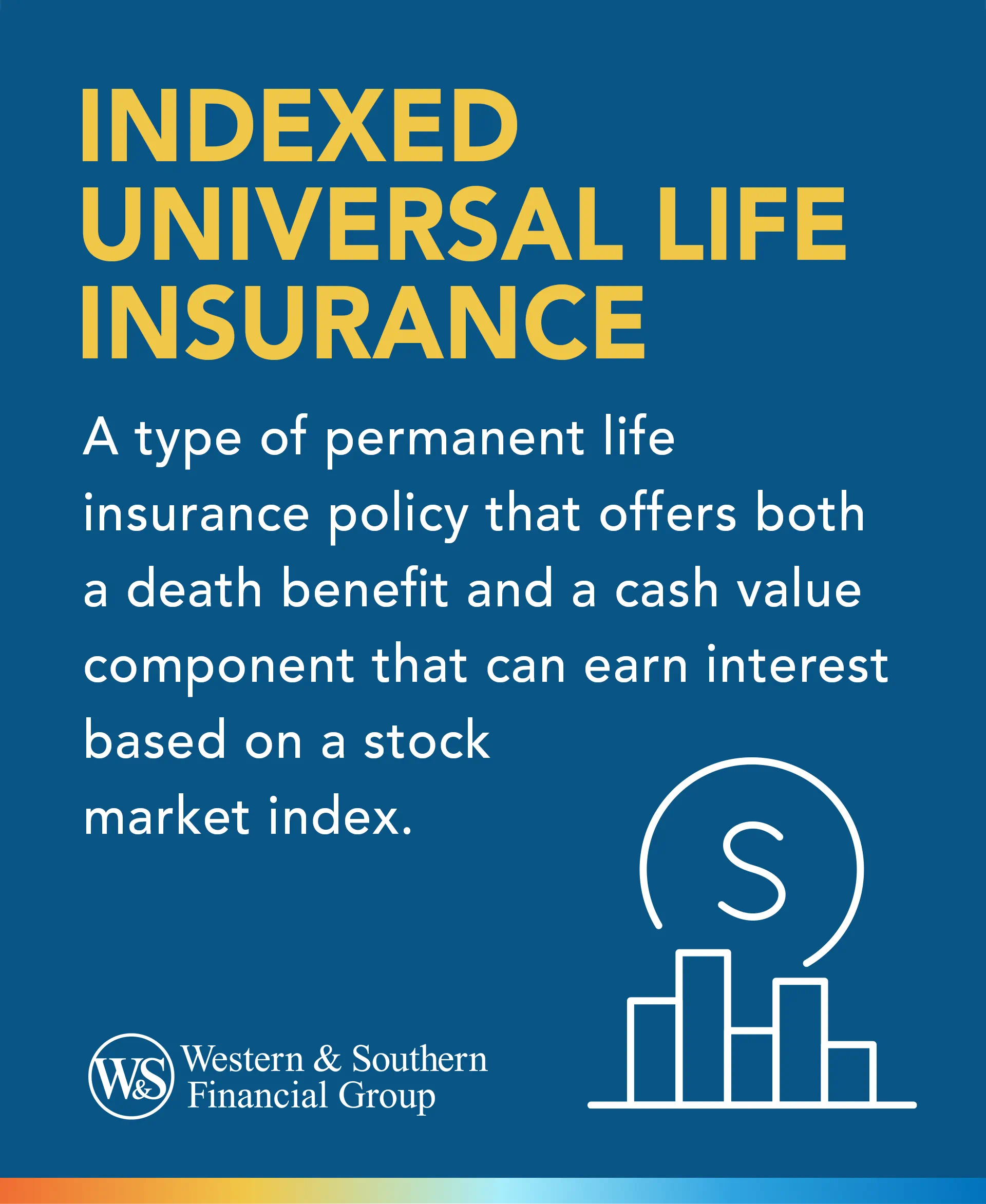

An IUL plan can provide you with the same type of insurance coverage security that a irreversible life insurance policy plan does. Bear in mind, this sort of insurance coverage stays intact throughout your whole life much like other long-term life insurance policy policies. It also enables you to construct money value as you age through a stock exchange index account.

Best Variable Universal Life Insurance Policy

Bear in mind, though, that if there's anything you're unclear of or you're on the fence about obtaining any type of type of insurance policy, make sure to get in touch with a professional. In this manner you'll recognize if it's cost effective and whether it fits right into your economic strategy. The cost of an indexed universal life policy relies on numerous aspects.

You will shed the death advantage named in the plan. On the various other hand, an IUL comes with a fatality benefit and an added cash money value that the insurance holder can obtain against.

Indexed universal life insurance coverage can assist you meet your household's requirements for monetary protection while additionally developing cash money value. Nonetheless, these policies can be much more complex compared to various other sorts of life insurance policy, and they aren't always ideal for every single financier. Speaking with a knowledgeable life insurance policy representative or broker can assist you determine if indexed global life insurance policy is a good suitable for you.

No issue just how well you intend for the future, there are occasions in life, both anticipated and unexpected, that can affect the monetary health of you and your loved ones. That's a reason for life insurance.

Things like potential tax obligation increases, rising cost of living, financial emergency situations, and preparing for occasions like university, retirement, and even weddings. Some kinds of life insurance coverage can assist with these and various other issues as well, such as indexed global life insurance, or merely IUL. With IUL, your plan can be a funds, because it has the possible to develop value over time.

An index may impact your rate of interest attributed, you can not invest or straight get involved in an index. Here, your policy tracks, however is not in fact spent in, an external market index like the S&P 500 Index.

Universal Benefits Insurance

Fees and expenditures might minimize policy values. This passion is locked in. So if the marketplace decreases, you will not lose any passion due to the decrease. You can also choose to receive fixed interest, one collection foreseeable rate of interest rate month after month, despite the marketplace. Due to the fact that no solitary allotment will certainly be most effective in all market environments, your monetary specialist can assist you determine which mix may fit your economic objectives.

Because no single appropriation carries out ideal in all situations, your financial professionalcan help you determine which mix may fit your economic goals. That leaves extra in your plan to possibly keep growing gradually. In the future, you can access any readily available money worth through plan fundings or withdrawals. These are earnings tax-free and can be utilized for any purpose you desire.

Talk to your financial specialist regarding exactly how an indexed universal life insurance coverage policy could be part of your general financial method. This material is for general educational objectives only. It is not intended to provide fiduciary, tax, or lawful recommendations and can not be used to stay clear of tax obligation charges; neither is it planned to market, promote, or advise any kind of tax obligation plan or plan.

Best Indexed Universal Life

In the occasion of a gap, impressive plan lendings in excess of unrecovered expense basis will certainly undergo normal income tax. If a policy is a modified endowment contract (MEC), plan lendings and withdrawals will certainly be taxed as regular earnings to the extent there are incomes in the policy.

These indexes are criteria just. Indexes can have different components and weighting methodologies. Some indexes have multiple variations that can weight components or may track the effect of rewards differently. Although an index might affect your passion attributed, you can not purchase, straight join or receive reward settlements from any one of them with the policy Although an exterior market index might influence your passion attributed, your plan does not directly take part in any supply or equity or bond investments.

This material does not apply in the state of New york city. Warranties are backed by the monetary stamina and claims-paying capacity of Allianz Life Insurance Firm of The United States And Canada. Products are issued by Allianz Life Insurance Policy Business of North America, 5701 Golden Hills Drive, Minneapolis, MN 55416-1297. .

Cost Universal Life Insurance

The info and summaries contained below are not planned to be full summaries of all terms, problems and exclusions suitable to the services and products. The precise insurance policy protection under any type of nation Investors insurance product goes through the terms, conditions and exclusions in the actual plans as issued. Products and solutions defined in this website vary from state to state and not all products, coverages or solutions are readily available in all states.

Your present internet browser could restrict that experience. You might be making use of an old browser that's in need of support, or setups within your internet browser that are not compatible with our website.

Universal Life Premium Financing

Currently using an updated web browser and still having problem? Please offer us a telephone call at for further aid. Your present internet browser: Detecting ...

{kind=link}

Latest Posts

What Is A Group Universal Life Insurance Policy

Tax Free Retirement Iul

Index Ul Vs Whole Life